Financial Wellness Is Now a Top Employer Priority — and It's Reshaping Health Programs

Workplace wellness used to mean a gym reimbursement, a yoga class on Thursdays, and a poster about hand-washing. That model is being retired. A structural shift is underway in how employers define employee health, and financial stress is now sitting at the center of it.

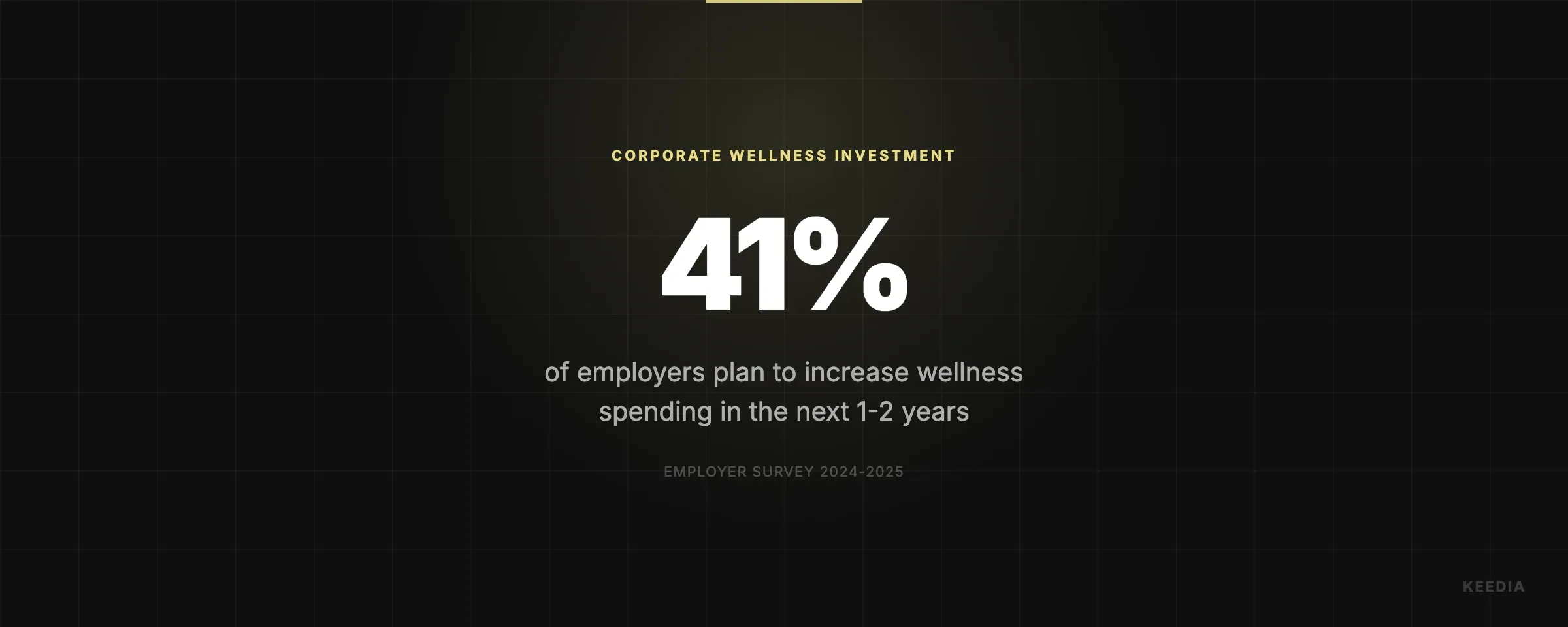

According to recent industry data, 41% of employers plan to increase wellness spending over the next one to two years. The three priorities driving that investment are mental health, preventive physical health, and financial wellness. If you work in fitness or corporate wellness, that last item on the list should change how you think about pitching programs.

Why Financial Stress Is a Physical Health Problem

The connection between financial pressure and physical health isn't abstract. It's physiological. Chronic financial stress triggers sustained cortisol elevation. That's not a minor inconvenience. Prolonged cortisol exposure is associated with immune suppression, disrupted sleep architecture, and a measurably higher cardiovascular disease risk.

Sleep disruption alone carries serious downstream consequences for physical performance and long-term health. Research published in 2025 found that poor sleep reduces muscular strength by up to 12%, a finding with direct implications for any employee population trying to maintain physical health while managing financial anxiety.

Cardiovascular risk compounds the picture. Employees under chronic financial stress show elevated inflammatory markers and blood pressure patterns consistent with sustained sympathetic nervous system activation. This is the same biological pathway that makes cardiovascular-protective interventions like sauna increasingly relevant in the employer wellness context. It's also why treating physical and financial wellness as separate silos misses the actual mechanism.

The practical implication: an employee who is financially stressed isn't just distracted. They're operating with a chronically dysregulated stress response that undermines sleep, recovery, cardiovascular health, and immune function. Gym access alone doesn't fix that.

The Numbers Behind the Shift

This isn't anecdotal. The data on employer priorities has moved sharply in a short window.

- 41% of employers plan to increase wellness spending within the next one to two years.

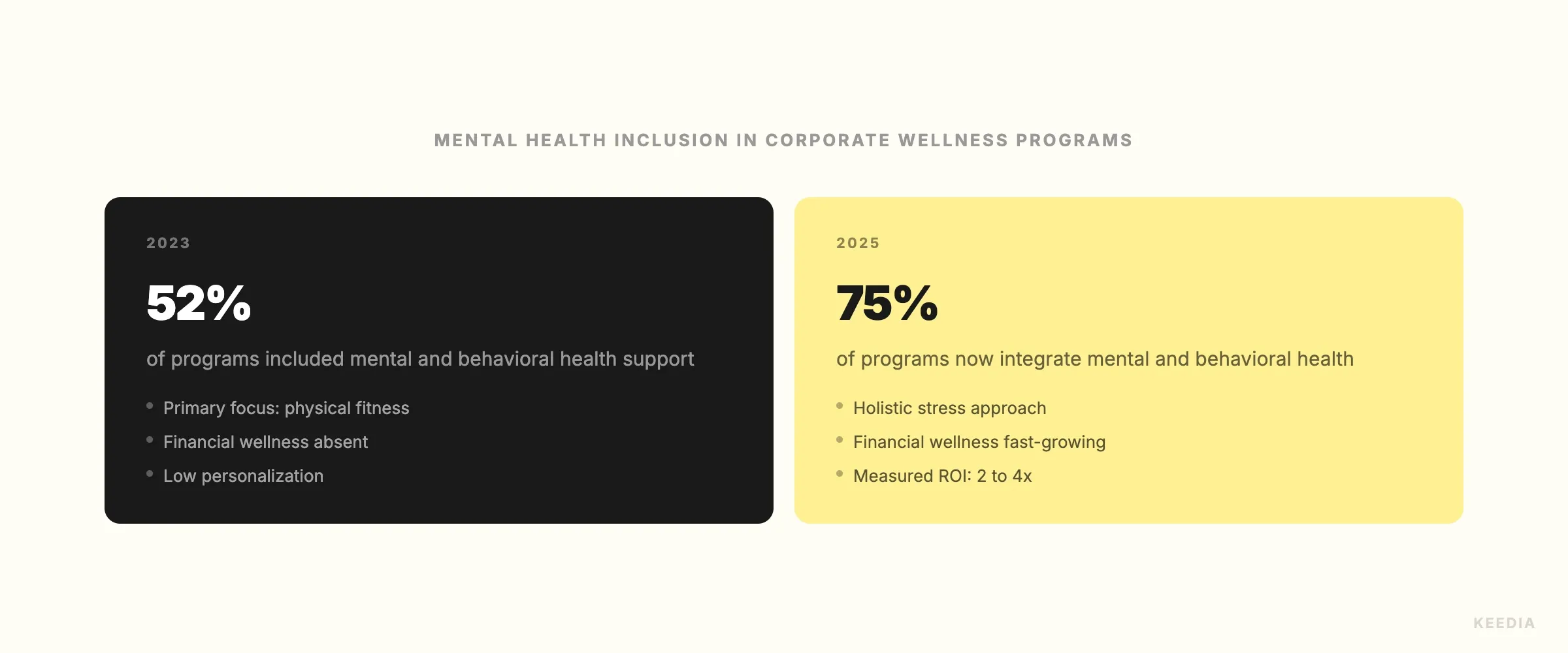

- 75% of corporate wellness programs now include mental and behavioral health support, up from 52% in 2023. Financial wellness is following the same adoption curve.

- US corporate wellness spending benchmarks at $150 to $600 per employee per year. High-investment companies report a 2x to 4x return on investment through reduced absenteeism and improved productivity.

- Adding financial wellness components to an existing program does not proportionally increase cost. It typically integrates into existing digital platforms, EAP structures, or workshop formats that employers are already funding.

The ROI case matters because it's what moves budget decisions. Data from Wellhub's 2026 workplace wellness analysis reinforces the productivity argument. Employers aren't increasing wellness spending out of altruism. They're doing it because the business case for a healthier, less stressed workforce is now well-documented.

Who's Actually in the Workforce Now

Any wellness program ignoring financial stress is also ignoring the primary health concern of the dominant workforce cohort. Gen Z and millennials now make up the majority of working adults in the US, UK, Canada, and Australia. Across all available survey data, financial stress ranks as their top health concern. Not back pain. Not nutrition. Financial stress.

This is not a fringe concern. These cohorts entered the workforce during or after the 2008 financial crisis, carry higher average student debt loads than previous generations, and have built careers in a period of significant housing cost inflation. For many, baseline financial anxiety is simply the normal operating condition.

A corporate wellness program that offers a standing desk stipend and a meditation app subscription is not meeting this workforce where it is. Employers who understand this are already moving. Those that don't will face increasing difficulty positioning their benefits packages competitively, particularly as talent competition for younger workers intensifies.

What Financial Wellness Programs Actually Look Like

When employers say "financial wellness," they're not talking about a pamphlet on opening a savings account. The programs gaining traction have real structure and measurable engagement metrics.

Current models include:

- On-demand financial coaching: One-on-one sessions with certified financial counselors, often delivered through digital platforms already embedded in employer benefit stacks. Common topics include debt management, emergency fund building, and navigating employer retirement matching.

- Financial literacy workshops: Live or recorded sessions covering budgeting frameworks, tax basics, and benefits optimization. These are frequently bundled alongside existing wellness programming.

- Emergency savings programs: Employer-facilitated automatic payroll contributions to short-term savings accounts. Evidence suggests even small emergency funds ($500 to $1,000) significantly reduce the psychological burden of financial stress.

- Student loan assistance and debt support tools: Particularly relevant for younger employee populations, these programs address the financial stressor most correlated with anxiety in the 25-to-40 age bracket.

- Integrated EAP financial counseling: Many Employee Assistance Programs are expanding their financial counseling component beyond the two or three sessions historically offered.

The through-line in all of these is stress reduction, not wealth creation. The goal isn't to make employees rich. It's to reduce the chronic low-grade financial anxiety that is actively undermining their physical health and cognitive function at work.

What This Means If You're Pitching Corporate Wellness

If you're a fitness professional or wellness consultant building a corporate pitch, the old template is being outpaced by what employers now need. A proposal that leads with gym subsidies and group fitness classes is still useful, but it's no longer sufficient on its own.

Here's what the updated pitch needs to do.

Connect physical programming to stress physiology. Your fitness offering should be framed explicitly as a stress-response intervention, not just a physical health benefit. Resistance training, zone 2 cardio, and recovery modalities all have documented effects on cortisol regulation and sleep quality. That's your direct line to the financial stress conversation. Employers now understand that these outcomes are connected.

Position your offering within the broader stress-health framework. You don't need to deliver financial coaching yourself. But your proposal should acknowledge financial and mental health stressors as drivers of the physical health outcomes you're addressing. A pitch that only talks about musculoskeletal health or fitness benchmarks is leaving the employer's actual problem unaddressed.

Speak ROI fluently. The $150 to $600 per employee per year benchmark is your entry point. Know what your program costs per head, know what absenteeism reduction looks like in dollar terms, and be prepared to discuss how your offering complements rather than competes with other wellness priorities employers are funding. Emerging data on structural workplace changes is increasingly being cited in these conversations, and staying current on it positions you as a credible partner rather than a vendor.

Know your retention data. Employers are sophisticated buyers now. They want to see engagement rates, program completion, and outcome tracking. If you don't have that data yet, building it into your next pilot is essential. Understanding what drives early dropout in wellness programming is directly relevant to making the corporate case, because engagement at 90 days is a standard metric employers use to evaluate whether a program is actually working.

The Bigger Picture for Wellness Professionals

The structural shift happening in corporate wellness is good news for fitness and wellness professionals who are willing to expand their frame. Financial wellness becoming a top-three employer priority doesn't threaten the case for physical health programming. It strengthens it, because it creates a shared language around stress physiology that connects everything employers now care about.

Mental health, financial wellness, and preventive physical health are not three separate programs running in parallel. They're three expressions of the same underlying risk: chronic stress and its downstream effects on human performance and health. Fitness professionals who understand that are positioned to offer something far more compelling than a gym reimbursement admin service.

The employers increasing wellness budgets are looking for coherent programs that address how their workforce actually experiences health. That's a significantly larger opportunity than the one the old wellness model created. The question is whether the fitness and wellness industry moves fast enough to meet it.