Peloton Acquires Skōp: What the $7,995 Pilates Bet Means

Peloton just made its clearest statement yet about where connected fitness is heading. The company's acquisition of Skōp, maker of a $7,995 connected Pilates reformer, isn't a distraction from its core business. It's a deliberate repositioning toward the premium boutique-at-home segment that its existing bike and tread lineup can't fully address.

At exactly the same moment, Crunch Fitness launched Crunch Reform Pilates inside its mainstream gym locations in June 2026, dropping reformer Pilates onto the budget-accessible gym floor for the first time at scale. These two moves didn't happen in a vacuum. Together, they bracket the entire Pilates market and force every brand operating in between to answer a difficult question: where exactly do you stand?

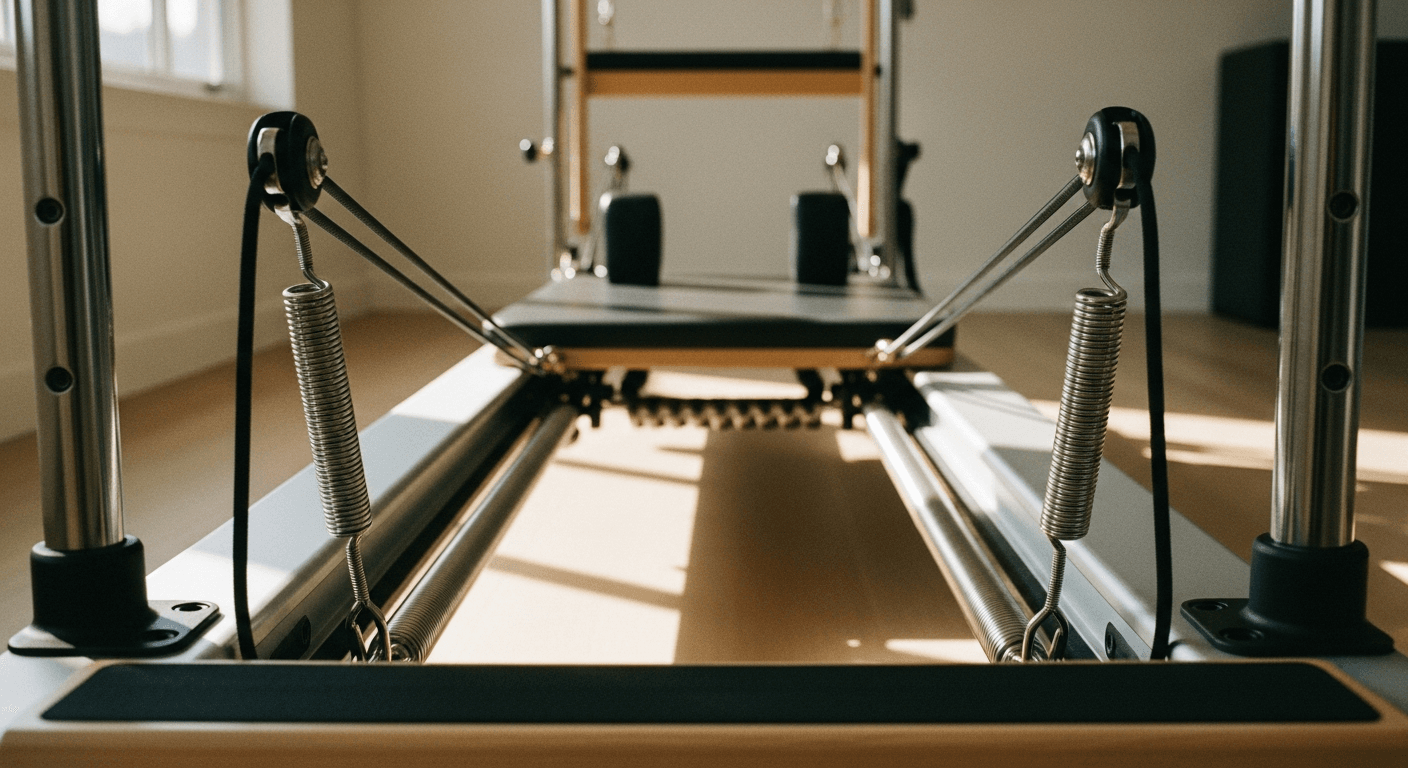

What Skōp Actually Brings to Peloton

Skōp's reformer isn't just a piece of hardware with a screen attached. The company built its IP around a combined system: the physical reformer, proprietary resistance mechanics, and a content library designed specifically for that form factor. That's the bundle Peloton is buying.

Building that stack from scratch would take Peloton three to five years minimum, assuming it could attract the right instructors and build meaningful class volume before the category moved on. Acquiring Skōp compresses that timeline to months. The M&A logic here is the same playbook that's worked across adjacent categories: buy hardware-plus-content IP rather than attempt to build it internally, and deploy your existing distribution to scale it faster than any standalone brand could.

Peloton's content distribution flywheel is the real asset it brings to this deal. The company already has millions of subscribers conditioned to pay recurring fees for fitness content. Attaching that flywheel to Skōp's hardware gives the reformer a monetization path that Skōp could never have accessed independently. It also makes the $7,995 price point more defensible, because the hardware becomes an entry point into a subscription ecosystem rather than a one-time purchase competing purely on specs.

Crunch Reform Pilates and the Other End of the Bracket

While Peloton moves upmarket, Crunch is doing the opposite with equal conviction. Crunch Reform Pilates launched inside existing Crunch locations in June 2026, using the chain's 400-plus location network as a mass distribution channel for a modality that previously lived almost exclusively in boutique studios charging $35 to $50 per class.

The Crunch model converts reformer Pilates from a premium boutique experience into a gym floor amenity included within a standard membership. That's a fundamental category disruption. It doesn't just compete with boutique Pilates studios. It redefines the value proposition of the modality itself for a large segment of the population who were never going to pay boutique rates to begin with.

This dynamic mirrors what's already playing out across the broader gym industry. The bifurcation between high-value low-price operators and premium boutique concepts is well documented. As Mark Mastrov's return to 24 Hour Fitness signals about the HVLP market, the middle-ground operator without a clear positioning is the one under the most pressure. Pilates just arrived at the same crossroads, faster than most in the category expected.

The K-Shaped Bifurcation, Now Inside a Single Modality

What's happening in Pilates right now is a compressed version of a structural shift that's been building across fitness for several years. The K-shaped fitness economy describes a market where premium and budget segments grow simultaneously while mid-tier operators get squeezed. You can read a detailed breakdown of how this plays out for independent operators in the K-shaped fitness economy and where independent coaches win in 2026.

Until recently, reformer Pilates sat almost entirely in the premium boutique tier. The modality's cost of delivery, the equipment requirements and the instructor-to-client ratios involved, made mass-market delivery structurally difficult. Crunch solved the structural problem by embedding reformers inside existing gym infrastructure, eliminating the standalone studio cost model entirely.

Peloton solved the opposite problem: it made the premium home version of the experience feel like an ecosystem rather than a capital purchase. Both solutions are coherent. The brands that don't have either solution are the ones who should be paying close attention right now.

What This Means If You're Competing in the Reformer Space

If your business sits anywhere near reformer Pilates, whether you're a boutique studio operator, a connected equipment brand, or an independent instructor building a client base around this modality, the competitive landscape just changed in a measurable way.

On the premium end, you're now contending with Peloton's content library, its marketing budget, and its subscriber base attached to Skōp hardware. That's not a competitor you outspend. The only viable response is differentiation on dimensions Peloton can't easily replicate: community depth, instructor relationships, in-person coaching, or specialization in populations that generic content doesn't serve well.

On the budget end, Crunch's 400-plus location network gives reformer Pilates a floor-space footprint that no boutique operator can match through organic growth. But Crunch is offering volume, not depth. The clients who leave a Crunch reformer class wanting more, wanting personalization, programming, and real progression, are the clients a boutique operator or independent coach can capture and retain. Understanding why clients leave personal trainers even when the training is good matters more in this environment, because the churn dynamic from mass-market exposure to specialist providers is real and exploitable.

The middle position, a mid-priced connected reformer without strong content or a mid-priced boutique without a clear differentiation story, is exactly where pressure concentrates when a market bifurcates. That's not a prediction. That's the pattern that has repeated across every segment of the fitness industry over the past decade.

The M&A Signal for Connected Fitness Brands

Beyond Pilates specifically, the Skōp deal sends a clear signal about how connected fitness M&A will function in the next growth cycle. The category of boutique-at-home premium equipment, devices that replicate a specific studio modality with proprietary content, is growing faster than legacy connected fitness (bikes, treads, rowers) as that segment matures and faces subscriber saturation.

Reformer Pilates, barre, functional training rigs, boxing. These modalities each have boutique studio customer bases that have demonstrated willingness to pay premium rates for a specialized experience. Any of them could follow the same hardware-plus-content acquisition logic that Peloton applied to Skōp. The brands that have built both the hardware and a credible content library are the acquisition targets. The brands that built hardware without content, or content without proprietary hardware, are in a weaker position when a strategic buyer arrives.

This also matters for independent coaches thinking about their revenue structure. The hybrid model that combines in-person sessions with digital content and remote programming is, in structural terms, the same bundle that makes Skōp worth acquiring. You're building a content-plus-delivery system. The hybrid coaching business model and how to structure it for scalability applies whether you're a solo coach or a boutique studio operator thinking about how to protect your position.

The Population That's Actually Driving Pilates Growth

One dimension of this story that deserves more attention than it typically gets: reformer Pilates has become one of the most effective entry points for older adults into structured movement. Its low-impact nature, the controlled resistance, the emphasis on alignment and core stability, makes it genuinely accessible for people who've been told by their joints that high-intensity training isn't viable anymore.

This population is large, growing, and underserved by generic connected fitness content. Research continues to show that structured resistance and mobility training delivers measurable longevity and functional benefits well into older age, which is exactly the promise a reformer delivers when programmed well. The evidence on starting strength training after 60 and the documented benefits for late starters underscores the size of this opportunity for operators who program specifically for this group.

Peloton's content flywheel will eventually reach this population. But a generic library built for a broad subscriber base won't serve them as well as programming built specifically around their needs. That's a gap that boutique operators and specialist coaches can own if they move deliberately.

Where This Leaves the Pilates Market

Peloton's acquisition of Skōp and Crunch's launch of Crunch Reform Pilates are not opposing forces accidentally colliding. They're the logical endpoints of a bifurcating market arriving at its natural destination. Premium home hardware with subscription content at $7,995 and above. Mass-market gym-floor access included in a standard membership. Both are coherent, scalable, and backed by distribution networks that individual operators can't match on their own terms.

The opportunity that remains sits precisely in the gap between them: the client who wants more than a gym floor class but hasn't committed to a $7,995 home purchase. That's a real segment. It's the same client base that boutique fitness built its first growth cycle on. Serving that client well, with depth, personalization, and programming that compounds over time, is still a viable business. But it requires being explicit about that positioning now, before the two ends of the market finish drawing the boundaries.