PersonalHour's Funding Push: AI Pilates Eyes Scale

On May 29, 2026, PersonalHour announced a new growth funding initiative built around three core pillars: AI-powered Pilates technology, home fitness infrastructure, and digital wellness experiences. The move signals more than a single brand raising capital. It outlines a commercial blueprint that investors across the connected fitness space are increasingly backing.

If you're building or evaluating a fitness brand right now, PersonalHour's funding architecture tells you where the money is moving and why.

A $22B Market Looking for Its Next Layer

The home fitness equipment market reached $22 billion in 2026. That's a large number, but it also reflects a market that has largely matured at the hardware level. Selling a reformer, a bike, or a rack is no longer the differentiator it was in 2020. The brands capturing investor attention today are the ones treating the device as an entry point rather than the product itself.

PersonalHour's three-pillar structure reflects this logic directly. Hardware gets you into the home. AI coaching keeps the user engaged. The digital subscription converts that engagement into recurring revenue. Each layer depends on the others, and that interdependence is precisely what makes the model defensible.

For a deeper look at how the smart home gym category is reshaping operator strategy, the operator response to the $2.44B smart home gym segment is worth understanding in full context.

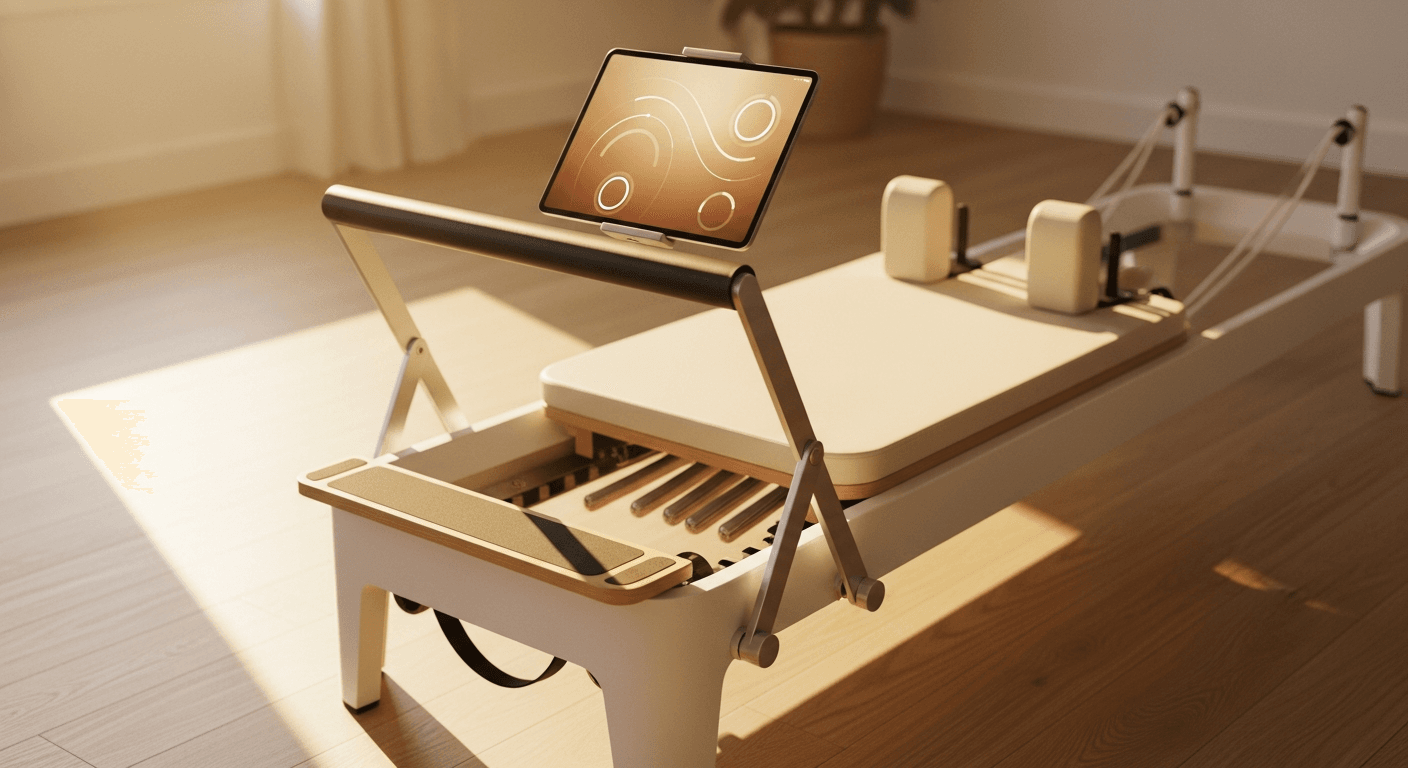

The Peloton Blueprint, Applied to Pilates

Peloton proved the model works: sell a connected device, then build a content and coaching layer on top that users won't easily abandon. PersonalHour is applying that same architecture to Pilates, a segment that has seen sustained post-pandemic growth and remains underpenetrated at the connected hardware level.

Pilates participation rates surged after 2020 as boutique studio attendance migrated toward home alternatives. The reformer, historically a studio-only piece of equipment due to cost and size, has become more accessible as brands invested in home-scaled versions. That shift created the hardware cold-start problem: manufacturers had a device to sell but no ecosystem to retain buyers after the initial purchase.

PersonalHour's funding push is a direct answer to that problem. By building personalized AI coaching, smart workout recommendations, and digital education into the platform, the company transforms a one-time equipment purchase into an ongoing wellness relationship. That's the recurring revenue play, and it's where margins in connected fitness actually live.

Why Investors Are Backing the Bundle

The investment thesis behind PersonalHour isn't complicated. Standalone equipment companies face margin compression and high churn. Standalone app companies face customer acquisition costs that rarely justify lifetime value at scale. The bundle solves both problems simultaneously.

Device revenue funds hardware development and reduces payback periods. Subscription revenue compounds over time and improves unit economics. AI coaching reduces the need for expensive human instructor hours while increasing personalization, which drives retention. When all three work together, the business looks far more attractive to growth-stage investors than any single component would on its own.

This isn't unique to PersonalHour. Look across the wellness investment landscape in 2026 and you see the same pattern repeating. Cymbiotika's $25M raise demonstrates how wellness brands that build layered, multi-touchpoint models are commanding premium valuations regardless of the specific category they occupy.

The Boutique-to-Home Migration Is Still Accelerating

One of the structural forces working in PersonalHour's favor is that the boutique-to-home migration in Pilates hasn't plateaued. Premium Pilates classes in US studios regularly run $35 to $50 per session. A committed practitioner doing three sessions per week is spending $400 to $600 per month before any merchandise or membership fees.

A connected home reformer with an AI coaching subscription can deliver a comparable experience at a fraction of that cost on a monthly basis, once the hardware is amortized. That value proposition is compelling enough to attract the high-income, health-focused demographic that Pilates has historically served. It's also a demographic with strong subscription compliance, which matters enormously for LTV modeling.

The post-pandemic fitness consumer has also become more sophisticated about programming. They're not looking for a workout video library. They want adaptive coaching that responds to their progress, flags technique issues, and adjusts difficulty in real time. AI makes that possible at scale in a way that pre-recorded content simply can't replicate. The 2026 Personal Training Industry Report makes clear that personalization is now the primary driver of retention across every fitness delivery format.

What This Means for Brands Building Their Own Roadmap

If you're a fitness brand evaluating where to invest over the next 18 months, PersonalHour's model offers a clear framework. The question isn't whether to build a digital layer. It's whether you can sequence the investment correctly so that hardware, software, and coaching reinforce each other rather than compete for resources.

Here's what the PersonalHour approach suggests for brands at different stages:

- Early-stage hardware brands should treat their device as the acquisition vehicle and begin building the subscription infrastructure before launch, not after. Retrofitting a coaching layer onto an existing product line is expensive and rarely produces the same retention outcomes as designing for it from the start.

- Digital-first coaching brands considering a hardware play should evaluate whether their existing user base has sufficient demand signal to justify the capital required. Hardware manufacturing is a different risk profile than content production, and the cold-start problem is real.

- Established fitness brands with existing equipment lines should be assessing AI coaching integrations now. The window for differentiating on connectivity is still open, but it's narrowing as more players enter the space with native AI architectures.

For coaching businesses specifically, the subscription pricing structure matters as much as the product design. Subscription pricing models that generate reliable recurring revenue are the financial foundation on which a connected wellness platform has to be built, whether you're an individual coach or a scaling brand.

The AI Coaching Layer Is the Real Moat

It's easy to underestimate how significant the AI coaching component is relative to the hardware. The reformer is manufacturable by multiple suppliers. The content library is replicable with enough budget. But a proprietary AI coaching model trained on user movement data, workout completion patterns, and physiological response signals becomes genuinely difficult to replicate over time.

Every session a PersonalHour user completes makes the model smarter. The dataset compounds. The coaching quality improves. And the switching cost for the user increases because no competing platform has their history, their preferences, or their baseline movement data. That's a durable competitive advantage built session by session, not through a single product launch.

This dynamic is increasingly well understood by institutional investors. Brands that own proprietary behavioral data alongside a physical product have fundamentally different valuation profiles than those that don't. The data layer is what separates a fitness equipment company from a wellness platform, and that distinction matters enormously when it comes to exit multiples and partnership opportunities.

The Broader Signal for Connected Fitness

PersonalHour's funding announcement lands in a market that is actively consolidating around bundle models. The Playlist and EGYM merger is another signal that connected fitness infrastructure is moving toward fewer, better-capitalized platforms with integrated hardware and software ecosystems. The standalone players in every segment, whether that's equipment, content, or coaching, are facing increasing pressure to either bundle or be acquired.

For Pilates specifically, the timing is well-positioned. The segment has genuine growth momentum, a loyal and high-spending user base, and relatively low penetration of AI-assisted connected hardware compared to cycling or running. PersonalHour is entering with capital at a moment when the competitive landscape is still forming.

Whether the company executes on all three pillars with equal success remains to be seen. But the funding structure it's announced reflects exactly the kind of integrated thinking that the 2026 fitness investment market is rewarding. Device plus data plus coaching. That's the formula, and PersonalHour is building to it deliberately.

If your brand isn't asking the same questions about its own architecture right now, that's the more pressing issue to address.