Zwift Acquires ROUVY: What It Means for Indoor Cycling

On April 29, 2026, Zwift confirmed the acquisition of ROUVY, the Czech-based indoor cycling platform known for its real-route video overlays. Both platforms will continue operating independently, with separate subscription packages and distinct product roadmaps. The deal is quiet in its announcement but loud in its implications.

This isn't a merger in the traditional sense. It's a consolidation play. Two of the most recognized names in indoor cycling software now sit under one corporate umbrella, and if you're a gym operator, a connected fitness brand, or a competing platform, the dynamics of your market just shifted.

Two Platforms, Two Distinct User Motivations

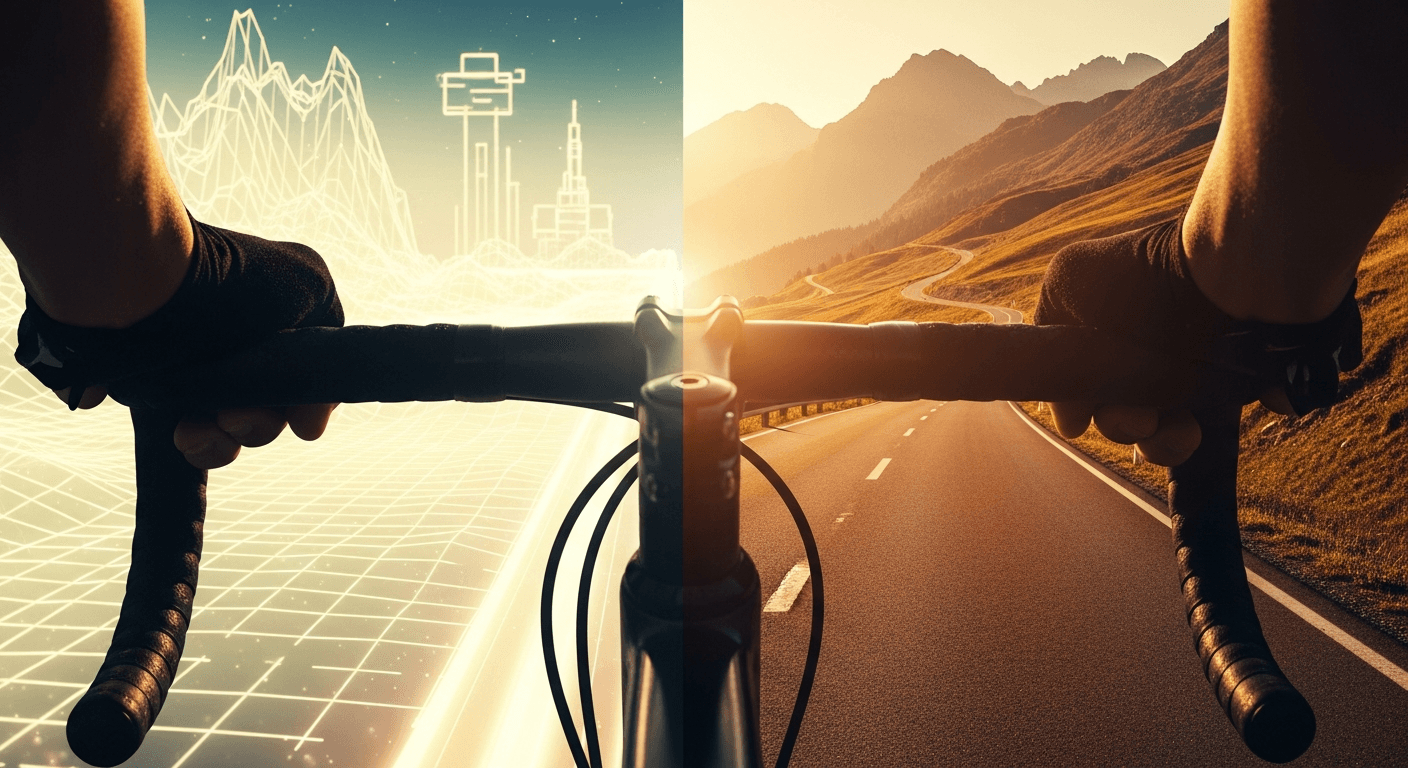

Zwift built its audience on gamified virtual worlds. Riders race through Watopia, earn experience points, and compete in structured events that blur the line between fitness app and video game. Its appeal is social, competitive, and deeply habitual. Zwift's subscriber base skews toward performance-focused cyclists and triathletes willing to pay a premium for structured training with a community layer.

ROUVY takes a different approach entirely. Its augmented reality video overlays place riders on real routes, from Alpine climbs to coastal road races, syncing resistance to actual gradient data. The experience is immersive in a documentary sense rather than a gaming sense. ROUVY appeals to riders who want to virtually pre-ride a race course, explore real-world terrain, or simply avoid the psychological fatigue of staring at an animated avatar.

By keeping both products intact, Zwift now covers two fundamentally different user motivations without cannibalizing either subscriber base. That's a strategically cleaner outcome than a forced platform merger would have produced.

The Land-Grab Logic

Indoor cycling as a software category lives and dies on subscriber retention. Hardware is commoditized. Smart trainers from Wahoo, Garmin's Tacx line, and a dozen smaller manufacturers all run on open protocols. The stickiness is in the software, specifically in the training content, the social infrastructure, and the habitual loops that keep users logging in weekly.

Zwift has faced real pressure on that front. After a pandemic-era surge that pushed indoor cycling adoption to record levels, the category cooled. Retention became the primary economic lever, and the competitive field fragmented. TrainerRoad leaned into structured training plans and AI-driven adaptation. ROUVY expanded its route library aggressively. Wahoo's own software ecosystem deepened. The result was a market where no single platform had a commanding lock on the casual-to-serious cyclist spectrum.

This acquisition changes that calculus. Zwift now holds a dominant position across two of the most differentiated user experiences in the category. If you're a cyclist who wants gamified competition, you're likely on Zwift. If you want realistic terrain simulation, you're likely on ROUVY. The combined entity controls both doors into the room.

Zwift's Positioning Shift: From Gaming to Mass-Market Fitness

Zwift has been explicit about its broader ambition: to make more people more active more often. That framing is a deliberate pivot away from its origins as a niche cycling game for enthusiasts. It positions Zwift as a fitness utility with mainstream appeal, closer to Peloton's brand positioning than to a competitive esports platform.

The ROUVY acquisition accelerates that shift. Real-route video content has a wider emotional pull than virtual worlds for the general fitness consumer. Someone who has never raced a bike but wants to virtually ride the Amalfi Coast or the Great Ocean Road is a larger addressable market than the performance cyclist chasing watts. ROUVY's content library is an on-ramp for that audience.

This matters for gym operators and fitness professionals because it signals where indoor cycling software is heading: toward broader health and wellness positioning, not deeper gamification. The research supports the demand. Studies consistently show that variety in training stimulus improves long-term adherence, and platforms that can deliver experiential variety, whether through routes, events, or formats, will win the retention battle. Why Mixing Up Your Workouts Adds Years to Your Life explores that adherence dynamic in depth, and it maps directly onto what differentiated indoor cycling content is designed to solve.

Concentration Risk for the Indoor Cycling Stack

Here's where the story gets complicated for operators and connected fitness brands. The indoor cycling software stack has just consolidated significantly. If you're running a gym with a cycling studio, your software partnerships now flow through a single entity controlling two of the top platforms. That's a meaningful shift in negotiating leverage.

Wahoo, TrainerRoad, and Tacx (now fully integrated into Garmin's ecosystem) remain independent, but their collective market share in the premium indoor cycling segment is smaller than the combined Zwift-ROUVY footprint. For gym operators evaluating digital cycling experiences for members, the options that can match that footprint's content depth and community scale are narrowing.

The parallel in the physical gym space is worth noting. When large operators pursue aggressive consolidation, as seen with VivaGym's acquisition of Synergym across Iberia, the market response tends to be a mix of competitive pressure on independents and accelerated platform standardization. Software consolidation in indoor cycling follows a similar logic. Smaller platforms either differentiate sharply or risk being squeezed to the margins.

For operators specifically, concentration in the software layer raises a practical question: what happens to your partnership terms if the primary vendor holds dominant market share? Pricing power, content licensing fees, and co-marketing arrangements all look different when your negotiating counterpart controls most of the category. If you're currently evaluating your digital fitness stack, this is the moment to stress-test your vendor diversification. HFA's FIT Tracker benchmarking tool gives operators a data framework for evaluating member engagement metrics that can inform those software decisions.

What Competing Platforms Need to Do Now

TrainerRoad's strongest card is its structured training engine and its AI-driven plan adaptation. It serves a specific, high-commitment user who values performance outcomes over entertainment. That's a defensible niche, but it's a niche. The broader casual-to-intermediate market that Zwift and ROUVY now jointly serve is a harder space for TrainerRoad to compete in on experience alone.

Wahoo's software play is tightly integrated with its hardware ecosystem. That vertical integration creates loyalty among Wahoo device owners, but it caps the addressable market at hardware buyers rather than platform-first subscribers. As smart trainer commoditization continues, hardware loyalty becomes a thinner moat.

For any platform looking to carve out defensible ground, the clearest path is probably in the professional and coaching layer. Structured, coach-mediated training experiences that connect athletes to real coaches are harder to replicate at scale and carry stronger retention characteristics than self-directed app experiences. The coaching software market is projected to reach $13 billion by 2035, and platforms that build strong integrations into that layer will be harder to displace. Coaching Software Hits $13B by 2035: How to Choose Wisely breaks down what that market growth means for platform selection and integration strategy.

The Health Angle You Shouldn't Ignore

Beyond the competitive dynamics, there's a genuine public health dimension to this acquisition that deserves acknowledgment. Indoor cycling is one of the most accessible forms of cardiovascular training available to adults across age groups and fitness levels. Research consistently links sustained cardiorespiratory fitness to reduced chronic disease risk across the lifespan. The evidence on how cardio fitness in your 20s predicts long-term disease risk underscores why platforms that reduce friction to regular cycling activity aren't a trivial category.

If Zwift's combined entity can genuinely expand the number of people completing regular indoor cycling sessions, the downstream health impact is meaningful. That's not marketing language. It's the actual case for why software that makes exercise more habitual and more enjoyable is worth taking seriously as a health infrastructure investment.

What to Watch Next

The immediate post-acquisition period will be telling. Watch for whether Zwift introduces shared login or cross-platform subscription bundles. A combined subscription offering would be the clearest signal that the two brands are moving toward a unified commercial strategy rather than a purely portfolio-based holding structure.

Watch also for how ROUVY's route library and hardware partnerships evolve. If ROUVY begins integrating Zwift's social and event infrastructure, the differentiation between the two products could blur faster than current messaging suggests.

For gym operators, connected fitness brands, and competing platforms, the window to negotiate favorable terms, build alternative integrations, and develop proprietary content moats is open right now. It won't stay open indefinitely. The Zwift-ROUVY combination is a consolidation move, and consolidation moves tend to accelerate, not pause.

The indoor cycling software category just got more concentrated. How you respond to that in the next twelve months will shape your positioning for the rest of the decade.