Crunch Franchisee CR Fitness Raised $350M to Open 100 More Gyms

In October 2025, CR Fitness Holdings closed a $350 million investment round led by Sixth Street, one of the most active alternative asset managers in the US. The deal positions CR Fitness to open more than 100 new Crunch Fitness locations over the next five years. If you run a gym, independent or franchised, this transaction tells you something specific about where institutional capital is going right now.

CR Fitness is already the largest Crunch Fitness franchisee in the country. It operates 93 locations across Florida, Georgia, North Carolina, Tennessee, and Texas, serving more than one million members. The company is targeting 110 locations by the end of 2026, with Arizona named as the next major expansion market. That's not incremental growth. That's a declared land grab.

What the Capital Stack Looks Like

The $350M round from Sixth Street is equity-focused growth capital, but it doesn't stand alone. The deal also includes a new senior debt facility provided by Golub Capital, which adds structured leverage on top of the equity injection. North Castle Partners, a private equity firm with a long track record in health and wellness, remains the largest shareholder in CR Fitness and continues to back the business.

This isn't a single check from one optimistic investor. It's a layered capital structure with multiple institutional parties who have conducted serious due diligence on the value fitness segment. When Sixth Street, Golub Capital, and North Castle Partners all agree that CR Fitness deserves this level of capital at this moment, you should read that as a consensus signal, not a coincidence.

For context on how similar institutional consolidation is reshaping adjacent wellness sectors, the Q1 2026 M&A activity in sports supplements shows the same pattern: capital flowing toward scaled, defensible businesses with predictable recurring revenue.

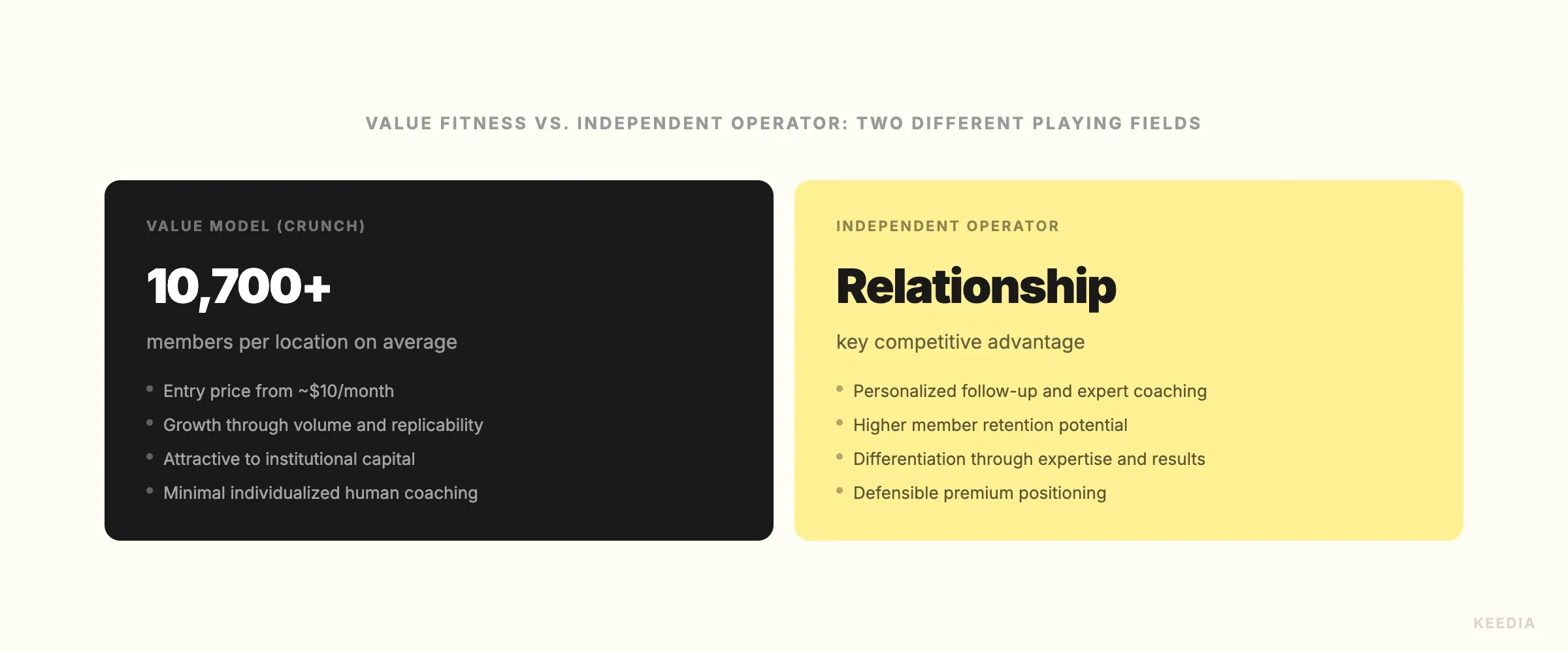

Why Value Fitness Is Winning Right Now

Crunch operates at a price point that is deliberately accessible. Basic memberships start well under $30 per month in most markets. That pricing is not a discount play, it's a strategic position. And in the current economic environment, that position is attracting members who are reconsidering more expensive gym commitments.

Healthcare costs in the US have continued to rise through 2024 and 2025. Discretionary spending is under pressure for a significant portion of the American middle class. Consumers aren't abandoning fitness, but they're auditing what they spend on it. A gym at $25 per month is a much easier retention conversation than one at $150 or $250 per month.

This is the structural tailwind behind CR Fitness's growth. Crunch's value model gives members a reason to stay even when budgets tighten. That predictability in membership retention is exactly what institutional investors want to see before committing $350 million. Speaking of retention, 2026 gym retention data makes clear that price sensitivity is now one of the top drivers of churn, which means value-priced operators have a structural advantage in member stickiness.

The math is also simple at scale. One million members paying even $20 per month generates $240 million in annual recurring revenue before any upsells, personal training, or ancillary services. Institutional investors understand recurring revenue models. That's why fitness businesses built on high membership volume and low monthly price are increasingly attractive compared to boutique operators with smaller member bases and higher per-head revenue.

The Expansion Playbook CR Fitness Is Running

CR Fitness is not improvising this expansion. The playbook is methodical. Florida, Georgia, North Carolina, Tennessee, and Texas are all Sun Belt states with population growth, favorable real estate conditions, and large working-class and middle-class populations who index well for value fitness membership.

Arizona is the logical next move. Phoenix in particular has seen significant population inflows from California and other high-cost states. These new residents are often budget-conscious and already accustomed to gym membership as part of their lifestyle. They're the ideal Crunch customer.

The 100-club expansion target over five years is aggressive but not unrealistic. At that pace, CR Fitness would need to open roughly 20 locations per year. For a company with the operational infrastructure already in place across 93 clubs and $350M in fresh capital, that cadence is achievable. It also parallels models like the one analyzed in depth in the piece on Workout Anytime's counter-cyclical franchise growth, where standardized operations and lean real estate footprints allow for rapid multi-market scaling.

What This Means for Independent Gym Operators

Here's the direct read for anyone running an independent gym or a smaller franchise operation: the capital flowing into value fitness at this scale will eventually touch your market. It may already have.

CR Fitness opening a 20,000-square-foot Crunch club with top-tier equipment, a sauna, group fitness classes, and a $24.99 per month membership within five miles of your facility is a competitive event you need to plan for. The question is not whether this is happening. The question is what your positioning is when it does.

You have two real options. The first is to compete on price, which is a fight you're unlikely to win against an operator with $350M in capital and the economies of scale that come with 100-plus locations. The second is to compete on something Crunch structurally cannot offer: depth of relationship, personalization, coaching quality, and community.

Boutique and independent operators who are winning in markets where value-price clubs operate are doing so because their members are paying for an experience and a relationship that no $25 per month membership can replicate. That means investing seriously in coaching quality, member outcomes, and the kind of programming that keeps people engaged. Research on connected gym equipment partnerships like the one between Les Mills and Life Fitness points to how even mid-size operators can build differentiated training environments that a large-format value club cannot easily reproduce.

Retention is also where independent operators can win. A high-volume, low-touch model like Crunch's is optimized for acquisition, not depth of relationship. If your coaching staff knows every member's name, their training history, and what motivates them, you're offering something that doesn't show up in a franchise's unit economics. Understanding what drives early member dropout is critical here, and the research on churn triggers in the first 90 days gives operators a concrete framework for building the kind of early relationship that drives long-term retention.

Private Equity and the Value Fitness Thesis

The CR Fitness deal is not an isolated event. It fits a broader pattern in which private equity and institutional credit are concentrating in fitness businesses that have two specific characteristics: accessible pricing and franchise-scale infrastructure.

Planet Fitness, which pioneered the high-volume, low-price model at a public company level, demonstrated that this segment can generate durable revenue across economic cycles. CR Fitness and Crunch are running a variation of that playbook with a more diverse facility format and a broader class and amenity offering. Sixth Street is betting that the model has significant runway in markets that Planet Fitness hasn't saturated.

What PE investors are not currently rushing to back, at the same capital scale, is the premium boutique segment. Studios charging $35 to $45 per class face ongoing pressure on both acquisition and retention. Some will survive and thrive through genuine differentiation. But the institutional capital signal is clear: value wins in a cost-conscious environment, and franchise infrastructure makes value businesses scalable.

For operators thinking about their own positioning, it's worth noting that the programming quality at your facility, including how well you structure training for real results, remains a genuine differentiator. Members who see measurable progress stay. That's why evidence-based programming decisions matter at the business level, not just the training level.

The Bottom Line for Gym Operators

CR Fitness raising $350M is a data point, not just a news item. It tells you that institutional investors see a long runway in value-priced, high-volume fitness. It tells you that the Sun Belt is the primary battlefield for this expansion. And it tells you that franchise scale plus accessible pricing is a formula that attracts the kind of capital most independent operators will never access directly.

Your response to that reality should not be panic. It should be clarity. Know exactly who your member is, why they chose you over a $25 per month alternative, and what you're doing every day to deepen that reason. The operators who thrive alongside the CR Fitness expansion will be the ones who stopped trying to compete on price years ago and started competing on outcomes, relationships, and community instead.

That's a harder business to build. It's also a harder business to displace with a $350 million check.